It's completely plausible that the post-Brexit Deutsche Bank is undervalued by the market due to panic and uncertainty, and Snapchat is overvalued by the market due to hype.

On Facebook v. Ford, in terms of how shareholder value gets built and sustained, yes, the market is being as rational as it ever gets. Consider the following five dimensions:

CREATING THE PRODUCT: Facebook's engineers provide the framework, but each day's content is created free of charge by 1.5 billion active users. That's great for profit margins! At Ford, cars don't get built unless the company buys steel, glass, tires, etc. and pays workers to put it all together. That really squeezes margins.

GENERATING DEMAND: Facebook's users share content and invite their friends to join, at no cost. Media companies beg to play in Facebook's ecosystem. By contrast, Ford needs to spend billions on advertising to get people excited about cars.

OBLIGATIONS TO CUSTOMERS: Facebook has a modest-sized fraud and security team that keeps everything tidy. They do heroic work, but there aren't 50,000 of them. At Ford, the requirements for inspections, safety tests, recalls, legal settlements when vehicles go bad, etc. are vastly larger.

OBSOLESCENCE: Ford has $58 billion invested in plant and equipment. Every day, those factories get a little closer to being obsolete. Ford must constantly either raise cash or reinvest profits to keep its factories competitive. That means less free cash for shareholders. By contrast, Facebook has just $8 billion invested in server farms, beautiful headquarters, etc. Its asset-maintenance burden is vastly less -- and should stay that way forever.

MAKING MONEY: Ford's net income zigzags all over the place, jolted by lots of market/economic issues. Net income was down last year; historically it's ranged from $11 billion to sizable losses. Facebook's net income totaled $3.7 billion last year and is climbing at a very snappy rate. 35% a year? Doubling? Still hard to tell, but it keeps going up.

Put all those factors together, and Facebook is a growth stock with a pretty straightforward path to making its business hum. Ford is a cyclical stock that may have already posted its peak profits. Ford may be a bedrock part of the U.S. economy, but that doesn't always get you a lot of love in the stock market, for reasons above.

Yeah, Ford has $150 billion in revenue a year and Facebook had just $18 billion. But markets value companies on their growth prospects. I've got no trouble believing that Facebook's overall opportunity to make money is 6x better than Ford's.

Shouldn't this analysis include the level of risk unique to a social network i.e. a usenet/myspace/digg/frendster crash?

Businesses that rely on and grow from network effects, die from them too at an even faster rate. A scandal or rival product could take FB to zero. Some would say that history tells us it is FB's inevitable outcome. I know some believe that it can't happen and the FB is "the last social network" but that sounds a little bit like bubble participants claiming "this time its different".

Interesting that you mentioned Foursquare. I considered them a has been for such a long time and only recently realized that they are still around being the geolocation API provider for a bunch of products. Successful pivot, I think.

My assumption was that it was never really a pivot. It seemed that the geolocation API was always their primary strategy. I thought that was why it continues to be odd that so much of Foursquare's usage and network loss seems attributable to their own consumer confusing actions to split out the social network part into a new brand (Swarm) instead of the other way around.

Great analysis but you left out one major point: Facebook is a monopoly in it's market segment, whereas Ford is one of many fierce competitors.

As such, Facebook takes all the profit from social media advertising, and can set its own prices and dictate terms to its customers. Ford can afford to do no such thing.

If Ford were the only auto maker in the world, it would be a far more lucrative investment.

Anything's possible, but the "It's just X" argument can be invoked so universally that I'm not sure it adds to the conversation.

ExxonMobil is just oil. WalMart is just department stores. Visa is just credit cards. All those companies have top-20 valuations. It's possible to come up with a doomsday scenario for any industry ... but by and large, once they get really big, they tend to persist in some form.

I made my point. If internet advertising is an overvalued sector of the economy -- which it most certainly is -- then all your favorite companies need new business models. What more do you want to hear?

Why do you think internet advertising is overvalued?

It is only this year that internet advertising is projected to match TV advertising spend. TV advertising has been around ~50 years, and before that we have another ~100 years of print advertising to learn from.

From those historic precedents we can see that advertising is a huge, huge market. It is true that something could surpass internet advertising as the best way to spend that money, but I don't see any viable candidates (I'm including mobile & VR ads in "internet").

AdBlockers - of course - accelerate the trend of the money in the "internet" category going to players like FB where they control the delivery mechanism (ie, deliver ads in a mobile app, where an ad blocker can't reach it on most platforms).

There is no tautology and no conflict. Both would be true statements of their conditional claims were true. The trouble is that internet advertising is far more likely to be overvalued than cars are. I think everyone in the thread knows this and is just being a bit difficult for some rhetorical purpose.

Perhaps I am wrong about this, but it was my impression that increases in internet advertising revenue were mainly based on increased volume, not higher prices. I don't see any reason volume should drop when more and more consumers are using the internet and spending more time on it.

Consumers don't buy advertising. Companies do. Consumers don't want advertising at all, and they don't really understand that all their tech products/services are subsidized by ad revenue. Would they pay recurring fees for those products/services without an ad subsidy? Some would, but most won't. So if and when companies (that actually produce something) decide that their investment is better spent outside of search and social media, and if consumers don't then fund those products directly, it will be like an earthquake in SF. This is exactly what happened to newspapers, by the way.

Internet advertising spending replaced newspaper advertising. What is going to replace internet advertising? VR? Those ads will probably still be sold by FB and Google.

To me, Google and FB's PE ratios are sensible, taking into account current profits, continuing growth in the short and medium term, and uncertainty in the long run.

The insight the parent offered though is pointing out the tautology in the former case. Because while everyone knows Ford == cars, lots of people see SV/Google and miss that most of it is in the selling ads business and much less in selling tech.

That very much depends on the context of the ad business in question. What stage it's at in terms of expansion and so on. Google zoomed right through the great recession, growing its advertising business while most businesses were struggling. As far as Google's business was concerned, the great recession hardly happened at all.

That's a good list, though I'd add a few caveats / contras to it.

Your "Creating the Product" and "Generating Demand" elements synergise off one another. Facebook has considerable network effects, and those network effects stimulate content, but break the chain, or boil-off customers (see "The Evaporative Cooling Effect"), and the feedback's strongly negative all the way down. MySpace imploded quite rapidly. Google's G+ had some traction initially, but worked exceptionally hard to drive off its strongest fans. Those who are slower to learn (/me raises hand) are only now being convinced of our error.

But "Obsolescence" is the big one. Ford's plant degrades from the inside, and the rate of amortisation of manufacturing equipment is fairly well known. Innovation in automobiles peaked in the 1920s, though it's arguable that there were additional spurts in the 1970s (largely around economy), 1990s (quality and electronic controls), and now a possible shift to hybrid or electric vehicles, though those remain tiny portions of the entire market (highly visible, but still tiny by either unit count or, slightly less so due to much higher per-unit costs, currency marketshare).

Ford, along with other US automakers was blindsided when a very modest amount of market innovation, toward more efficient vehicles, hit in the 1970s. That was an exogenous obsolesence function.

Facebook and other technologies face this all the damned time. As I've slowly realised, the cost of provisioning technology hardware falls by an order of magnitude per decade. The rate is much slower for software, but there's far more capable, far more modular software rising up all the time. You can actually see this progression going back to the dawn of electronic computing, with IBM owning the market in the 1950s and 1960s, then a cascade of first minicomputers (DEC, Wang, Sun), then micros (PCs), then laptops, now handhelds, coming along at roughly 10-year intervals.

Software's taken a while to catch up.

Facebook had roughly 1/10 the hardware cost profile of Google (though growth of the Web may have increased that). Scaling out a startup now is largely a solved problem. Revenue model is harder -- but you need far less revenue.

The other problem Facebook (and any other tech player) faces is that their own codebase becomes liability. For every table-based desktop site (say, Hacker News), that existing site layout (and perhaps much the technology underpinning it) actively impedes movement to mobile or tablet devices. I've had long arguments with designers of sites who insist on pixel- and point-based font sizing, rather than em and rem, and then screw up with low-contrast sites to boot.

(HN's own fonts are barely readable for me on a 10" tablet, and no, mobile extensions don't help.)

Further, "Making Money" for Facebook has been exceptionally reliant on both easy-money Federal Reserve policies, and lending and banking regulations favouring Silicon Valley style investments. A tremendous amount of advertising is itself financial services, electronics, and other startups (I'm basing this off of Google's advertisers which I'm familiar with from other sources, but suspect FB's profile is similar). That ads money could well dry up damned quickly.

Tech companies have the problem that as the money dries up so does their tech workforce. Look at the salaries reported to have been offered to Yahoo's top tech talent (if you can't offer appreciating stock, you've got to bleed money). Lose programmer interest, and again there's a downward cascade of talent and capabilities, and some of the negative feedbacks start dominating.

> But I'm at a loss to draw the correct conclusion from this. Is it rational that Facebook is now worth 6x as much as Ford?

I worry that I see it as over-hyped because of my discomfort in the future it proposes. Its valuation represents the market's belief in what I feel is a very dark future.

One of the many weird things about the stock market is that it doesn't really reflect how investors feel about a given company, so much as it reflects how investors are predicting how other investors will feel about a company in the coming years.

So, a slightly more optimistic way of looking at it is that investors think that other investors think that there's a dark future ahead, but may not believe so themselves. It's quite possible that no one really believes in that particular dystopian future, but everyone thinks that everyone else does.

My level of optimism depends on whether I think FB can make enough profit to sustain their current valuation based on their current advertising alone, or whether they'll need to broaden their horizons in terms of monetising the data they hold.

It's fairly easy to imagine monetisation strategies that could be pretty negative in the long term.

They could influence elections, shift social policy to help certain people, and generally engineer the social world in their own image. It will be very hard to tell if this is happening.

They could become the whole internet. In many places they already are. This is a very sad future for someone who sees the internet as a tool of human liberation and direct connection.

I don't care so much about them selling our information. It's worthless even to me. These other things are much more subtle and valuable.

According to me, yes. And mostly not doing enough stuff together and eye to eye -- which makes those words easier and less meaningful when they are not accompanied by actual effort, money, being there, etc.

Digital is a nice way to keep touch or contact new people, but bad replacement for physical socializing. Of course it's also easier and needs far less commitment, courage and empathy, and you can't beat that for people...

Facebook uniquely knows the social network, communications, whereabouts and psychological makeup of ~1 billion individuals across the world. They've demonstrated the power to manipulate their users' emotions. Ford manufactures motor vehicles in a highly competitive industry. Comparing early Ford to current facebook might be a better comparison as they were both heralds of new disruptive technologies.

It's more plausible that Europe is going to go through a much harsher next ten years than the last ten years have been (a time during which the EU and Eurozone both saw essentially zero net GDP growth). They've only added to their debt situation since the great recession, nothing has actually been fixed, and they will be unable to raise interest rates for the next decade at least - that combination will continue to suffocate all GDP growth, by locking up trillions in capital that will no longer be productive and will be stuck in a blackhole yielding a negative return for decades.

Italy for example is imploding on $300 billion in bad debts, which is likely to send their economy into a Spanish style depression. That's going to sink a lot of European banks. Deutsche Bank's lead economist is already calling for a $150 billion EU bank bailout. They're going to need something more like $500 billion as the financial picture gets worse in Europe in the next few years.

Finland as another example is in a nearly decade long soft-depression, and is likely to abandon the Eurozone as their situation will continue to drift and erode.

Countries like Sweden, Denmark, the Netherlands, and Norway, now have among the most indebted households on earth based on debt to income ratios. The mortgage debt accumulation going on there can't continue indefinitely.

Spain and Portugal have barely begun to pull out of the last recession, when a new one is inbound. Greece is still a hobbled mess.

Countries like France and Germany that are center to Europe's economy, have had zero growth for nearly a decade. Germany's ability to continue to bail out other parts of Europe, is now at an end.

It's far more likely Deutsche Bank will be quasi-nationalized, than not at this point. The next few years will be worse, rather than better.

I agree. Although in the case of banks, a panic can be self fulfilling. DB may be well capitalised and have sound assets, but if there is a market panic and no wholesale investor will roll their funding with them (as happened after Lehman went bust), and retail depositors start a run on the bank, the bank will go bust. Even if it is solvent.

The liquidity requirements introduced after Lehman should be sufficient for banks to sustain another Lehman scenario but you could imagine an even more severe stress.

The various Landesbanken (banks of the states), the Bundesbank (federal bank) and KfW (kinda the federal investment bank) will be kept afloat in some way (although there might be mergers, as there were in the past), since they're public entities.

However Deutsche Bank is a private company. It's still likely to be kept alive, but it's not as certain.

You are right that DB is private, nevertheless the bank is deeply intertwined with financing the Deutschland AG. Without them Daimler, BMW, Bosch, etc all would have to find new partners for financing their day to day operations.

>They let Greece go bust rather than the Landesbank.

It more a case they may have to bail out Greece rather than letting it default and take out the Landesbank.

A lot of the problems could be prevented by the German controlled ECB easing monetary policy and aiming for say 2% inflation rather than the present 0%.

As I like to point out whenever people claim that the ECB is controlled by Germany: Germany has a very small minority of the votes in the controlling gremium.

Influence in the Euro institutions is largely determined by the size of the economies and their contributions to the budget. Germany is first among equals.

I'm sorry - I don't mean to imply that Germany is all powerful. The power dynamics of different EU institutions are complex and sometime unwieldy. And often a single country can block something. However I respectfully disagree with your last sentence - assuming each country has equal power is not reality but fantasy.

As others have pointed out, the German government would probably be ready to bail them out if they ever ran into trouble, though that would likely be a painful process for existing common shareholders.

It's probable that they are both over valued. Deutsche Bank supposedly has insane amounts of derivative exposure and is highly leveraged. Then again if you assume that they will be bailed out at any cost you could be right.

Yeah, germany helping greece was mostly to save the over exposed DB, and I don't think it's over yet on that front. then there's the italian front, which is more of the same, and on top of it brexit has messed up euro value even further. It's going to recover, but that burned a lot of non indexed capital

Edit: For a more complete analysis of DB's capital position, they have published Moody's report on their credit. [2] I don't see much in there that would suggest DB was insolvent, but they do seem to be having some difficulty reorganizing their business.

The capitalisation of a bank is not based on its market value but on its accounting value, i.e. how much money shareholders brought in, and how much profits the bank retained over the years.

A falling share price doesn't impact the bank's capital ratios. It does impact however its capacity to raise more capital if required, which is not a good thing.

It was similarly surreal when WaMu disintegrated -- they sold their deposits to Chase for less than the amount of the deposits, which seems odd at first ("they just sold a pile of money for less than the money itself was worth"), but isn't really. WaMu couldn't just spend those deposits, they were only worth the amount of money that could be extracted in fees for holding the accounts and from invested the deposited money, which was naturally less than the value of the pile of money.

WaMu's $170 billion in customer deposits were "sold" to Chase for $1.9 billion (I thought both numbers were bigger, but so says Wikipedia). If you were a WaMu banking customer before the implosion, you were a Chase banking customer afterwards.

Again, you can't sell deposits. Chase assumed the business of WaMu, which included liabilities - mostly deposits. Deposits are a liability and it is impossible to sell a liability. So saying "they sold their deposits to Chase for less than the amount of the deposits" is entirely inaccurate. It's somewhat counter-intuitive because deposits "seem" like assets and loans "seem" like liabilities - but it's actually the other way around on the balance sheet.

DB may be insolvent, but to be fair, there aren't many banks that can pay out the figures recorded in the managed accounts. I recall one Utah bank which is supposedly able to, and there may be others, but usually a mainstream bank cannot fulfill 99% withdrawals of assets on short notice.

I don't think any bank can. But it's not a capital problem, it's a liquidity problem. A bank, whether an internationally active, or a mum and pop local bank, is in the business of taking short term deposits and lending the money long term. Banks are required to cover some of their deposits in liquid assets so that it can sustain some level of stress. But a full scale run on the bank where all depositors want their money back would kill any bank, big or small.

A bank is solvent, Madoff wasn't. Madoff didn't have any asset, the cash you would have invested with him had been used to pay off other investors.

A bank has assets, the money you lent the bank (through your deposit) is invested in a mortgage, backed by a property. You will ultimately get your money back. but it is a timing issue (and therefore liquidity), not a solvency issue.

It's a liquidity issue if the bank invested in mortgages (usually), but it can be a solvency issue if they are invested in debt (sovereign or corporate) that can be defaulted on.

Totally different. A bank generates a return on it's deposits.

Madoff just paid a dividend or phony appreciation to investors based on money deposited by new investors -- except for the money he stole it was a closed system with no return generated.

He also concentrated his efforts on courting a relatively insular community (religious Jews) via trusted community figures to avoid awkward questions.

Thats usually a sign of a scam -- banks don't send your priest/rabbi/community leader to hawk CDs. But there are many hustles (Ponzi schemes, pyramid schemes, and various savings clubs) that are common in ethnic and religious communitiesand apread via word of mouth.

I used to work in the financial institutions group at a buldge bracket bank doing valuation and M&A on the banks team. The thing about bank valuation that's weird, is that it's balance sheet valuation and not income statement valuation. Banks don't sell things, they sell money. The make money off interest earned on loans - their cost of capital (~interest paid on deposits=0) - branch/hr overhead (if they have branches). Anyways, to compare a bank to another company that sells physical goods or widgets is kind of silly to begin with. They are not valued the same way, and they make money completely differently.

I like to think that there are two extremes for valuations.

On one side of the range, the consulting firm, which has no assets, and which value is a pure function of future earnings.

On the other extreme you have an investment fund where the value is purely a function of the value of the assets which are all liquid financial assets. You don't buy the fund at a premium, otherwise you might as well buy the underlying assets yourself.

A bank is somewhere between the two. It has what should be a reasonably reliable accounting value since at the end of the day, all of its assets are financial assets that can be sold and aren't highly specialised like a factory or a hotel building is. But on the other side a large part of the value is not just the balance between assets and liabilities. It has additional earnings (fees, trading activities, etc).

Consulting firms generate revenues. Their assets are mostly human capital, but their value is generally a multiple of current earnings, not "a pure function of future earnings".

Most banks hold a decent amount of highly specialized, illiquid debts that have no active market and could reasonably be compared in terms of liquidity to real estate or capital goods.

I am not sure I understand your point. How is that different from what I wrote.

And no, there are no line in an IFRS balance sheet for "human capital".

[edit] and on your second point, I don't think I agree. You will pretty much always find a buyer for financial assets. Unless they are so rotten that no one thinks they are worth what you have them in your books for (which may be the case for some Italian banks).

Where I think you are right to be careful with banks is with the size. If you need to wind down a massive international bank, you need to find buyers for a awfully large amounts of assets, and that will likely damage their value.

> I am not sure I understand your point. How is that different from what I wrote.

Yeah, we are on the same page, it was just a little nit as it seems weird to me to state that future revenues are the "pure" base for valuation when future is informed by current. Just semantics though.

> You will pretty much always find a buyer for financial assets. Unless they are so rotten that no one thinks they are worth what you have them in your books

At the right price you will find a buyer for anything. I was speaking to your point about liquidity, which is not about price of the asset, but about the quantity of interested buyers and the ease of structuring and executing a transaction with a buyer.

But there are buyers for complex financial instruments. There are many hedge funds around who can do both size and complex products. And other international banks have the teams and system to buy a portfolio.

But size is a problem. When you have 2 trillions $ of assets to sell, even if they are simple vanilla mortgages, it will be a buyer's market.

> but their value is generally a multiple of current earnings, not "a pure function of future earnings".

Not sure what your objection is. The function is something like V = 3 * r, where V is the value of the company and r is the annual revenue. Boom, pure function.

Ok, but if I wanted to buy enough shares to own DB or snapchat (if it were public at its current valuation) I would have to pay more to own Snapchat. So while it doesn't make sense to compare underlying assets/liabilities, it does make sense when you ask the question: how much would I need to pay to own this business?

But Snapchat is not public and that makes a world of difference. Its valuation is based on a group of investors that likely have a totally different risk tolerance and time horizon that the market as a whole. The terms of their investment are also likely totally different than the terms you get as a standard shareholder of a public company. E.g. if they have liquidation preference, that's going to distort the valuation calculated based on their investments.

The article compares DB Market Cap to Snapchat's "valuation" which is based on the terms of its latest funding round. Snapchat doesn't have an Enterprise Value because it's not a public company, so the value of its equity is currently unknown.

As I said before the DB/Snapchat comparison is apples to oranges when you compare balance sheets, but both metrics (market cap, "valuation") are decent proxies for the magnitude and direction of the "true" value of the company.

Market cap is not a decent proxy of the magnitude of the value of the company.

EV in it's simplest form is Mkt Cap less Cash plus Debt. Just b/c a company isn't public doesn't mean the value of the equity is unknown.

If you buy the equity of a $100M company that has $90M in Net cash then you really are only paying $10M for it. Likewise, if the company had $1B in Net debt then you are paying $1.1B for it. Theoretically, DB could issue $10B of debt and buyback $10B of equity tomorrow and that reduces their mkt cap dramatically (their regulators wouldn't be too happy about it, though).

My point is that Banks use leverage so mkt cap is NOT a decent proxy of the value of the bank. When you compare valuation of 2 companies using Market Cap for 1 or the other (or both) is VERY misleading, especially when you have one that has a business model that uses leverage.

The real question: what does Snapchat's equity look like?

You practically need a PhD in finance to value these things, with all the preferences, participation multiples, board seats,drag-along and pro rata rights, etc attached to these shares...

It's the value of the equity (shares); market cap completely ignores debt.

Market cap is a good way to think about what the total value of a company's stock is, but a leveraged (indebted) company may have some of its "company value" "owned" by bondholders as well. EV is the total value, whereas MC is just the shareholders' part.

I feel like this shouldn't be a dumb question, but here it goes:

So, how come people are purchasing equity without paying any attention to debt?

I understand how different classes of shares may be equivalent in scenarios where a company is successful, but very different if it is failing. I also understand that the market has established a price for 0.01% of a company, and not necessarily a price for a much larger share.

Ha, I wonder what the students in that class thought when the instructors were "too dumb" to teach the consensus understanding in corporate finance.

That said, on Hacker News, subjects like company valuations seem to be discussed in terms that are more consistent with economics than what you typically hear from students of finance.

Completely different model, and banks are weighed down by projected losses on bad assets. But the image is still valid, "Look at this formerly formidable mega-bank which has less equity value than a disappearing picture and video app." (Of course it's not a public market valuation, and much of the assets are supported in debt) European banking has been suffering along with Europe.

Perhaps the bigger issue is that when banks get to such a low level of equity relative to debt, they have no cushion to absorb losses. Once the equity hits zero, they become insolvent and that's when the Lehman comparison becomes very valid.

Want proof that this is total mathematical coincidence and irrelevant....if DB were going to sell itself, do you really think they would include SnapChat in the comps table? No.

The guy who wrote that article is such an idiot. A reducing market capitalisation is not "shrinking the banks". It might mean the banks may be making less profits, but that doesn't make them safer, rather more dangerous on the contrary (as they can't climb their way out of a loss through earnings). Shrinking a bank means reducing its balance sheet, its leverage not its share price.

Totally, especially with leverage and a large notional insurance/derivitives liability. If reality moves in the wrong direction against that insurance and there's nothing but debt at the end to the payees, then too-big-to-fail cascade effects, ala late 2007, happen in the system again. This is why derivitives should be heavily regulated.

IMO, even the most libertarian government would not allow a normal insurance company take on so much leveraged potential liability without at least a disclosure to the consumer that says, "Hey, this company probably can't payout the policy you just bought from them." Yet somehow it's okay for financial instruments? IMO, Dodd-Frank should have forced financial institutions to calculate their overall liability on derivitives as part of their capital requirements. This would never happen though, as they trade so rapidly most banks probably don't even know at any given time what would happen to their derivitives liability if the market swung wildly, either up or down.

We're going to have another 2007 again, for sure. I have no idea when, but we did not solve the underlying problem at all.

> This would never happen though, as they trade so rapidly most banks probably don't even know at any given time what would happen to their derivitives liability if the market swung wildly, either up or down.

I think the technology is there to make it happen automatically. It's a deterministic system. The problem is the lack of political will to do so, which is appalling and leads to situations like Brexit and Trump.

Yeah, I like the illustration that Brexit is Bear Stearns especially because the market has recovered in the last two weeks(as it did with BS in 2007) and a DB implosion would be the Lehman Brother for the next collapse.

Why are any of those worth over a billion? Valuation should be assets - debts + future profits. In reality, mostly, it's psychology + voodoo magic - negative press.

I used to think this way, then I spent the last decade watching my friends all get rich working at these kinds of companies.

You need to look at the big picture here. Young people aren't watching TV. Ad spend by the likes of P&G, Nike, and the auto industry is still largely on TV. Also, Silicon Valley largely hasn't been able to capture brand advertising -- the spend on billboards, sports stadium advertising, etc vs. direct-response like Google AdWords. Ask anyone in the industry, they'll tell you direct-response spending is a drop in the bucket compared to spend on brand advertising.

Now, tell me, one the ad industry wakes up and realizes how absurd it is to dump billions of ad spend onto a platform with rapidly declining viewership (linear TV), where is all that ad spend going to go?

Maybe a communications platform that's used heavily by young people (great for advertisers), to send pictures and short videos (ads?) to each other in a playful, unhurried manner?

I don't know whether that's worth $20 billion or whatever its "valuation" is, but these dumb cheap shots against ad supported tech company valuation need to end. These platforms are as big as like, several big TV networks combined in viewership, with about 100x better ad targeting. How isn't that worth billions?

I wonder if a "scorched earth" plan could be pitched to old school TV advertising giants, in order to score billions for adblocker research. Adblocking has "needs AI" written all over it.

The point is that there won't be an all-cash 17bn transaction for Snapchat. I'm unaware of a SV startup sale in that dimension which happened in mostly cash. Usually, and I may be missing some deals, it's part cash and mostly shares of the buyer.

"Microsoft Corp. (Nasdaq: MSFT) and LinkedIn Corporation (NYSE: LNKD) on Monday announced they have entered into a definitive agreement under which Microsoft will acquire LinkedIn for $196 per share in an all-cash transaction valued at $26.2 billion, inclusive of LinkedIn’s net cash"

They acted quickly and avoided a worst-case outcome. As such it was effective.

However, arguably the bank bailouts could have had much better terms for the taxpayer - most of the upside was realised by bank shareholders who were not wiped out, rather than the taxpayer who bore the risk.

For comparison, Warren Buffet also recapitalised some banks in the depth of the crisis, demanded and got long-term warrants that paid out truly humongous amounts of money once bank shares rose back to pre-crisis levels. Tax payers - in comparison - got a few percent of interest rather than adequate compensation for the risk they bore.

Nothing terrible happened to the US economy, compared to past banking failures I would call that a success. However, it's really hard to compare such things across vastly different time periods.

That line is a whopper! All they managed to do was conceal fundamental problems a bit longer by offloading crap assets on the taxpayers. And, possibly, make the inevitable bank failures more spectacular and destructive when they do happen.

The effectiveness of the changes is subject to political interpretation. American banks are strong right now which indicates our policy decisions weren't bad. Whether they were good or not is debatable.

General argument of this story seems to be that "if an industry is not doing well in the open market it needs taxpayer doleouts to prop up share prices". Europe has tried that many times before (e.g. with the shipping industry) and it has always ended in tears... Let's not go down that road yet again!

> When the biggest bank in Europe's biggest economy, with annual revenue of about 37 billion euros, is worth about the same as Snapchat -- a messaging app that generated just $59 million of revenue last year -- you know something's wrong.

Snapchat is not 'worth' 17 billion. Some investors start to make money on the investment iff Snapchat exits or IPOs above 17b, but that's about it. The term 'valuation' is completely misleading when applying it to this 17b number.

In fact, due to liquidation preferences in the term sheets Snapchat's true valuation (i.e. the point at which investors actually lose money) immediately post investment, according to basic math, is $0.

I think Facebook would make a $17b offer, but that the actual number is significantly higher. Snapchat is much more of a threat to Facebook than Whatsapp and FB had no problem opening up the piggy bank to grab it.

The title seems to suggest that this due to the Brexit, but in reality the value of Deutsche Bank has been in decline since the financial crisis of 2007-2008.

The underlying dynamics of the two companies are quite different, and I'm not sure their "worth" can be directly compared.

One is worth a lot to the granny taking out cash from her pension fund, the other is worth a lot to the advertisers wanting to cash in on the cloud social services.

The pessimism around Snapchat in this thread is reminiscent of the negativity surrounding Facebook. Advertising is moving to social media, Snapchat is currently the best platform for targeting the demographic advertisers value the most (young people).

Central banks does not fix the economy. Maybe the Brexit was a analogy to poker play call on central bank strategy whatever it takes print new money as central bank debt.

Thanks for updating the title. I wonder sometimes if the residual malaise in the economy is about not writing off the bad loans. Cancel the loan, roll up the debt. Painful yes, and disruptive, but one way to recalibrate investment risk and to normalize capital flows more accurately.

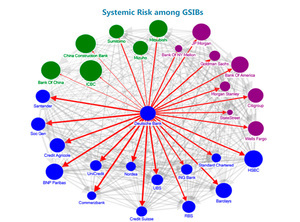

Comparing Snapchat with Deutsche Bank sounds like a (bad) joke. Snapchat could go bankrupt and everyone would laugh at it... DB will never go bankrupt and here's a simple pic that explains why:

It's another league. That could cause a x10 times Lehman. Too big to fail. If DB falls, the rest of the world follows suit...

Another pearl from the article:

> If the rot isn't stopped soon, Europe will have found a novel solution to the too-big-to-fail problem -- by allowing its banks to shrink until they're too small to be fit for purpose.

A bank failure doesn't have to happen overnight (Lehman), it can happen over a protracted period of time, in which there will be no systemic risk to the global banking establishment. In 2007, every bank was playing dirty w/Credit Default Swaps + CDOs -> "if our balance sheet is loaded with garbage, then the other guy's is too" -> no lending -> credit crisis. The only thing the DB "has" that is toxic is crappy management. BoA won't reconsider it's lending to JPM Chase because of DB, as would've been the case in 2007.

A confirmed bankruptcy of Deutsche Bank would be followed by the collapse of 10s of banks, not in a day but maybe few weeks. Quick enough for unleashing the biggest financial armageddon in the western world.

> there will be no systemic risk to the global banking establishment [...]

Are you sure? on June 30th the IMF said exactly the contrary: "Deutsche Bank Poses Greatest Risk to Financial System"

Logic would have it that more money would pour into SV and VC in general. Say €500B new money is pumped into the Eurozone banks, where is that money going to go? The boom in VC financing post 2007 is by in large due to the surplus 'free' cash that was floating around the US and global economies due to quantitive easing. More money means more competition for equal amount of startups which points towards valuations being pushed even higher.

The relevance is that this is really shoddy journalism. It is slightly sensationalist and just plain wrong in its assertion that Lehman was the catalyst of the 2008 financial crisis. This is notable because Bloomberg is generally a respected news source for finance.

{kind=link}

{kind=link}