Yellen and the FDIC is in a tough spot. This is the important line, "Any losses to the Deposit Insurance Fund to support uninsured depositors will be recovered by a special assessment on banks, as required by law."

Thus, on one hand, I'm glad they're doing this, as it should help prevent wider bank runs, and it ensures that banks are the ones that are actually paying for it.

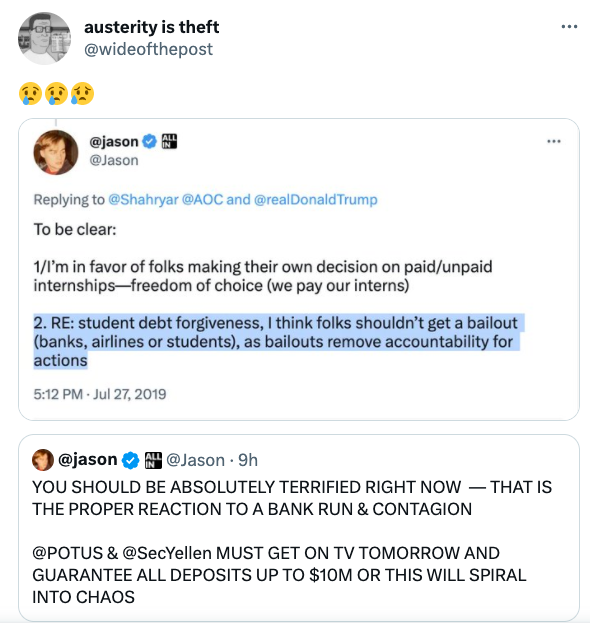

At the same time, this is yet another example of changing the rules in the middle of the game. Yellen has just broadcast that FDIC insurance is essentially unlimited, as long as you can threaten wider disruption to the economy.

I understand part of this is human nature but I really wish we could plan for these entirely foreseeable events ahead of time so that it's not just cases of "selective justice" with regards to who gets bailed out.

Banks have lost all excuses to be making money out of other people's deposits. If those deposits are guaranteed by the government, and backstopped by the government, then there's absolutely no reason banks should be able to invest any of them.

There's absolutely no excuse left for why banks get to invest any of their clients money. They get free leverage from their clients for free. They can send it to zero and the entire risk will be held by the government. That's absurd.

Revoke banks ability to invest deposits. They can't get to have the cake and eat it too. They could offer higher interest rates for non guaranteed accounts which bear risk, or zero risk for the already zero interest rates.

>If those deposits are guaranteed by the government, and backstopped by the government, then there's absolutely no reason banks should be able to invest any of them.

>Revoke banks ability to invest deposits. They can't get to have the cake and eat it too. They could offer higher interest rates for non guaranteed accounts which bear risk, or zero risk for the already zero interest rates.

You are missing something crucial here - treasury bonds are a loan to the government - this is all by design.

Who will loan the government tens or hundreds of billions of dollars besides the banks? The [Fed/Treasury/FDIC] has no incentive to prevent banks from loaning customer deposits, because the Treasury needs banks to purchase government bonds

> because the Treasury needs banks to purchase government bonds

Does it? Or is this just how the system is currently designed?

50 years ago we might have asked who will provide the Fed with the gold it needs to issue enough currency to avoid deflation as the population grows exponentially.

>Does it? Or is this just how the system is currently designed?

Yes, to both questions. The US Debt is at $31 trillion, it only works as long as the system keeps feeding money into government bonds.

The entire global financial system (not just the USA; the rest of the world is dependent on the USD and US banks) is reliant on this cycle of money.

>50 years ago we might have asked who will provide the Fed with the gold it needs to issue enough currency to avoid deflation as the population grows exponentially.

It was realized the gold standard stifled growth too much, and was abandoned just about 50 years ago as well.

You can have a safe system without growth (everything Tech was built off credit/debt and castles in the sky until decades after the companies were founded) or you can have the tech industry with a debt-credit based system.

That does not address the second question at all? The bonds need to be bought by someone, but you gave no argument why this someone has to be banks and why banks need tax money for bailouts on top of that.

It was explained, maybe you didn't connect the reasoning.

First, there are no entities that have the amount of capital needed to keep the bond market moving besides banks. This is a $50 trillion market that makes the stock market look like a lemonade stand. I would suggest you do some research on the bond markets, it will become immediately apparent why only central and private banks have the capital necessary to drive it.

It's the nature of a credit/debt based system, which is currently in a booming credit cycle (although perhaps the end of the cycle)

As to why do banks need tax money for bailouts?

The banks don't need tax money, if you're willing to let banks fail - which would likely be healthy in the long run.

But in the short term, Joe Middle Class can't get a car loan to get a car, Wealthy Sally can't get a business loan to start a company and employ 50 people, Minimum Wage Mike can't get a home loan after saving up money for 25 years.

It's certainly a shame that banks basically face no consequences and the taxpayer has to pay for it. But people's perspective on bank bailouts changes quickly when they realize the "side effects" are their credit cards no longer exist and their loan rates tripled.

The banks need to buy treasuries, because they treat bonds as a risk free financial instrument. Everyone else would have to recognize the risks inherent in those bonds and thus demand higher interest. The federal government can't afford that.

The reason why banks need to be bailed out, is because they treat treasuries as risk-free financial instruments. If they didn't get bailed out from time to time, they'd have to recognize the risk in buying treasuries.

So our banking system needs somewhere to park capital risk free, and it’s economically desirable that’s in a place that doesn’t create other distortions such as asset inflation or malinvestment. So we have treasuries as a tool for the financial system.

But there seems to be a premise in this thread that the US Gov needs (as in has no other possible choice, even via legislative change) to sell treasuries in order to fundraise.

I accept that’s sort of how the current system works in that effectively the US Gov creates capital/spend in the financial system via various programs and investments and attempts to offset inflationary effects / currency deflation effects by taxation and other revenue before finally encouraging other parties to allocate capital out of the system in the form of treasuries to make up the shortfall.

Effectively as I see it a treasury is then a promise not to spend capital for the term in exchange for the promise you’ll get the expected present value of that capital returned at the conclusion of that term (or in the case of TIPS/I-Bonds, the best approximation of the actual present value of that capital at that time).

Amongst other features, this neatly “allows” the US Gov to allocate an equivalent amount of capital to a purpose it considers appropriate while theoretically lessening impacts compared to simply spending that money without the offsetting treasuries.

But I’m not entirely sure there’s some sort of fundamental rule that the US Gov with the support of the Fed “needs” anyone to buy treasuries - together they could, as an example I’m not necessarily advocating, provide a safe haven facility for anyone who wanted it and continue to influence the monetary system and zero-risk rate of return (eg by the Fed paying interest on reserve accounts as they have since 2008) while otherwise having the Fed simply create the currency the government requires for deficit expenditure (eg by directly buying treasuries from the Gov if we perpetuate the illusion) and using other fiscal policy to control the inflationary/distortion effects of this spend.

That is, I’m not sure it’s the case that the US Gov exactly needs the banks to borrow treasuries because it could not afford them not to. Rather, the value of treasuries is as a measure to absorb excess liquidity, provide safe haven, and adjust risk behaviour in the financial system.

My open question is whether the current system is the only way, yet alone the best way, to practically achieve this goal?

you think inflation is a problem now, wait until Congress has the literal power to order the Fed the print money which is effectively what you are proposing.

I do not trust the Fed, but I Sure as shit do not trust the US Congress.

Paper money is a "Federal Reserve Note". It comes from the federal reserve not the Treasury

The Treasury creates coins or bonds. This is one of the reasons congress has floated the idea of the 10 trillion dollar coin. As it is within their power to order the Treasury to mont that. They can not order the federal reserve to make a 10 trillion dollar bill

Of course it is the fed who prints the money in the US and has dual inflation/unemployment targeting mandate. In other countries this role is typically performed by the central bank.

The debt ceiling doesn’t control spending because it is a misnomer. The money has already been spent. The debt ceiling controls whether the government will honor the obligations it has already made.

And that is cheaper? How much more expensive would a "correct" interest rate be compared to bailouts+economic fallout+loss of public trust you get from the current "risk-free" fantasy?

Trying to keep up the growth half a century ago was the last thing that (at least the West) needed to do - and it was already aware of that at that point.

I'm very much not saying that the outcome wouldn't be disastrous, but IME default is clearly unconstitutional, and so if statute and circumstance conspire to make default the only option then violating some statute to prevent default is appropriate, potentially to the point of just printing what we need to meet our obligations.

People can learn how to use Treasurydirect.gov instead of using their bank as a lousy bond broker. Inflation protected bonds, that you can buy only $10k a year of are some of the highest yielding risk free investments that exist. Banks should just make money off fees and hold short duration Treasury bills only.

Other institutions that have LPs should lend to businesses, students and home owners.

But then you don't have the convenience and liquidity of a bank account. The system works because the bank can invest the aggregate deposits of all depositors and still be ready to cash people out as needed (of course, barring a situation like this one, which is what the deposit insurance is for).

The majority of people don't need daily bank accounts. The only reason why we are using them is because to dollar notes have not kept up with inflation. A $500 bill from 1900 would be a $17,500 note today. Two of those notes provide more liquidity than the majority of bank accounts in the US.

>Who will loan the government tens or hundreds of billions of dollars besides the banks? The [Fed/Treasury/FDIC] has no incentive to prevent banks from loaning customer deposits, because the Treasury needs banks to purchase government bonds

War bonds were bought by people directly. I see no reason why we can't have the same today. God knows the US needs a WWII sized investment in repairing infrastructure.

Individuals purchasing war bonds helped, but didn't pay for WWII.

The war cost a little over $300 billion. $50 billion of that was through individual purchases of War Bonds, the rest came from banks and taxes.

Bankers and merchants have always funded the United States. A representation of Robert Morris, the "financier of the American Revolution" is painted in The Apotheosis of Washington, the fresco decorating the ceiling of the rotunda in the Capitol building where he is shown receiving a bag of gold from the god Mercury. Soldiers and supplies were paid for with "morris notes" which was a proto-currency of the US that was backed by Morris' personal fortune.

Yup. The reasonable UX here is that you as a retail customer get to pick what assets your deposits should go into, and you take the risk. Bank just gets a minor cut for doing the admin work.

And yes, that means if you picked “10y treasuries at 1.56% interest rate” back in 2021, then 80% of your deposit would now be gone. You should have picked “3m treasuries at 0.1% interest rate”.

This whole idea that a bank deposit is some magical asset that you can never lose anything on (other than through inflation) is a leaky abstraction. Like with all leaky abstractions the happy path is great, but when it starts leaking it can get real bad.

So people rather than banks would now be sitting on hundereds of billions of losses. Instead of depressing bank profits those losses would be depressing consumption or home purchases.

Depressing home purchases might well be a good idea. Right now people treat them as investments rather than mere housing, and as a result that market is thrown entirely out of whack.

Indeed, home prices increasing at more than a modest rate is a bad thing for everyone in the long term.

Homes should be investments in the same way that a factory or warehouse is an investment. You buy instead of renting in order to fix the cost of doing business over time, not to speculate on potential future values.

Yes, with "Land Bank" being a big thing now, with people just buying up land and holding it to simply fight inflation, things are just going to spiral out of control one way or another.

The US government already sells billions of dollars worth of various types of bonds to consumers every year. How is what you're proposing any different, and how would you entice more people to buy them than are currently buying T-bills, T-bonds, I-bonds, etc.?

Who is going to buy them? Most US citizens have less than a month's worth of income in their savings account. I'd be surprised if they enough confidence in their own income to tie even half of that up in war bonds.

Many (most?) Americans have no savings account. Not because they are poor but because a savings account is largely an obsolete anachronism. The common tactic of conflating "savings" with "having a savings account" is intentionally misleading.

Per the US government, the median US household has $1000/month they could invest after all ordinary expenses.

Perhaps we'll be forced to accept that we cannot continue to have "endless growth" with a declining workforce. The cost of Labor is going to go up at all levels, and that will mean smaller profits and more inflation until things stabilize and enough of us are incentivized to do productive work.

> Does this mean all American banks (indirectly bank customers) will pay to cover depositor losses that exceed insurance funds?

That assumes banks balance this liability by reducing payments to customers rather than reducing profits. That's a common and completely misleading claim by businesses - if they are taxed or fined, they pass it on to their customers (obviously, it's an attempt to create political support for the business).

The reality is that the ability to raise prices (or lower interest rates on deposits) depends on the elasticity. If you raise prices on your bottle of water at the supermarket, then people will just buy the bottle next to it - the water-maker will be paying and fee or tax increases out of their profits. If you have the only bottle of water in the desert, you can charge whatever you want. I would think that regular savings deposits, at least, are easily moved to another bank.

Another consideration is that if they could squeeze more out of customers, they'd probably already be doing it. By that theory, at least, they've already optimized or that and can't charge more.

> If you raise prices on your bottle of water at the supermarket, then people will just buy the bottle next to it - the water-maker will be paying and fee or tax increases out of their profits. If you have the only bottle of water in the desert, you can charge whatever you want. I would think that regular savings deposits, at least, are easily moved to another bank.

However, this fee is levied on all member banks of FDIC, which is basically every bank. Thus, it creates the most natural ground for collusion, i.e. everyone implicitly agrees to pass on the fees to the customers.

More than that, a bank account is probably one of the stickiest "purchases" an average individual makes in their lives, unlike a single-use water bottle. How many people do you think has the time and energy to switch to a new bank every time there is a fee increase? Is it the individual's fault for not doing so?

You're not supposed to talk about that! "If something we don't like happens we'll have to raise prices!" seems to be taken at face value all the time. It's true that in an idealised perfectly competitive market a measure which increases the costs of all producers equally will raise prices across the board, but this is absolutely not realistic.

As you say, the what really matters is (perceived) elasticity. If a company thought they could increase profit by increasing prices then they'd just do it. Conversely if they get fined or regulated or whatever but, as expected, it doesn't affect their elasticity curve then they'll leave prices where they are. If they were acting rationally it was already at the ideal point.

Normal/poor people don't put enough money into banks for it to represent much of their earnings. IIRC, from that image that was circulating around, much less than half of the deposits of even BofA are from accounts <$250k. So I don't think accounts like your grandma's are going to bear any percentage of the brunt of this.

> Normal/poor people don't put enough money into banks for it to represent much of their earnings.

This is hurtful in more ways than one.

Banks routinely charge all kinds of fees from account maintenance to whatever Wells Fargo did for years.

Retail banks won't let the Federal Reserve open a bank account for everyone by default with the Fed.

Either what you say is true and the retail customers are insignificant, and banks must offer no fee accounts. If not, they can't block federal reserve from creating default USD accounts for everyone.

Or they are an important part of the bank's marketing strategy or whatever. In this case, banks must lose the ability to gamble customer funds.

> Retail banks won't let the Federal Reserve open a bank account for everyone by default with the Fed.

Actually the FED is opposed to this themselves. A company called the narrow bank was going to try this. The FED refused them a banking license, all the way to court.

The FED wants deposits reinvested into the economy.

> A narrow bank takes deposits and invests the money in interest-bearing reserves deposited at the Fed. Because that’s all these banks would do, they would be very low cost and hence could pass along to depositors the interest earned on reserves, minus a small fee.

> Narrow banks could attract many large depositors, who currently receive much lower interest rates on their deposits at ordinary commercial banks.

It feels like they were offloading their cost to a service that the government maybe offers at a loss.

It's not so much about the loss, its about the fact that banks lose their depositors. It is great for an economy that the 'savings' of people are used to safely invest in good ideas. This is the function of banks, and incidentally a function that really benefits from a profit motive.

Hence I believe the Fed was against this to keep the economy running by 'keeping money rolling'.

I am not convinced by this argument* because banks can already do that. I don't think that bank are "required" to invest client's deposits, so they can already just stash paper cash in a big vault. It is clearly a dumb strategy for a retail bank.

This proposal for narrow banking seems to employ the government as this vault, sort of like treasury bonds that can be freely withdrawn, which seems a more significant difference.

* I am not denying that this is what the feds claimed and/or believed

It’s deposit volume rather than number of accounts that are over $250k. I’m sure that most of the accounts are <$250k, but a single $1m account accounts weighs the same as 100 $10k accounts.

> Yeah, the fees and lower interest rates from this will be pretty brutal for the poor.

I'm fairly sure the poor aren't that affected by interest rates - the very definition of being poor is not owning much in the way of assets that could earn interest...

It's not only the earned interest on savings being discussed here, the OP was also including higher interest rates on the variable rate loans that most poorer borrowers qualify for.

They only need to cover 20 billion or so for SVB? In the grand scheme of all banks, that's not a ton. SVB wasn't some FTX oops it's all gone level fraud.

Assuming it's a one time charge and not a contagion, it sounds like why we have government and FDIC.

An assessment on banks costs shareholders of the bank, not accountholders. (Maybe it indirectly costs accountholders if banks lower interest rates on customer deposits, but these rates are generally not affected by a small short term shock).

It might seem unfair that shareholders of random other banks have to pay for this but no more unfair than accountholders of SVB paying for it.

I don't have a crystal ball but I have a strong guess about which of these options are most likely to be implemented.

Not only will tax payers likely pay for this but the most likely tax payers to pay are the ones with the least flexibility (stuck with variable rate debt, limited banking choices, no dedicated money managers working on their behalf) aka the poorest tax payers.

If my assessment is correct, they have somehow found and settled on a solution more disgusting than a generally distributed tax payer bailout.

4) Banks get their privileges revoked and they are no longer an oligopoly with privileges of being the only way to store dollars legally, and the only investment institutions who get to gamble their customers money while the government is insuring their loses but does nothing about their gains.

The Fed releases a digital dollar that you can bank without needing to be a part of this oligopoly. Banks are forced to give better terms to be attractive again, terms that will make up for the risk of the bank using your money. Deposits are no longer guaranteed because being in a bank is now a deliberate choice instead of something you're forced to do despite having money.

Banking is not competitive in any way. The small players are very risky to bank at. The big players get to be riskier because they are protected by the government.

They got to play with 10x leverage with their client funds for free. You can't barely get 2x leverage at broker, you pay interest rates much higher and they actually enforce strict margins.

Minewhile these people out of their privilege as bankers got to play with much bigger leverage, while paying zero interest rates to their counterparty which turned out to be fully paid for by the government in the end.

100% investment loss in this case is hardly enough, with the leverage levels banks can access they can literally collect pennies in front of a train and have positive expectation values for shareholders, while investing in negative expectation value investments.

And they did collect pennies in front of a train. Bought 10yr treasuries at historical lows. They paid their customers nothing for it.

VC investment strategy for VC bank. They took the zero or hero attitude until the end. Again, we're taking about people with already VC mentality of "worst case 100% loss, best case 1000%".

No wonder that once VCs recognized their own shadow they fled so fast.

And now they are pretending as if it's the fate of the banking system on the line.

VC bank, managed like VC venture for VC firms. They deserve to lose VC money.

Their loans are probably also worthless than they claim, but they managed to successfully swindle the Fed in the most VC way ever with the shortest deadline. I'm betting FDIC is going to pay twice as much as expected in the end.

> And they did collect pennies in front of a train. Bought 10yr treasuries at historical lows.

> worst case 100% loss, best case 1000%

See I don't understand how you can have 1000% return by buying treasuries, at any time. It was a stupid decision in hind sight, but the best case is order of magnitudes below 1000% return.

And you've put these two things right next to each other, what am I missing?

They would be perfectly safe have they dumped their deposits into T-Bills.

They didn't went for the 1000%, they went for the 5-10% extra and ended up losing everything.

Had they used T-Bills or even straight up depositing it against the Federal Reserve for NO return, they would remain liquid and could now reinvest into higher yield bonds as the rates have risen. Instead they now hold 1.5% 10 year HTM bonds that are now valued at 70% original today because the prevailing rate is 4.5%.

To clarify I don't know the actual strategy they took. I am responding to how they can have risk in "make safe loans" or "buy safe bonds" scenario.

> They would be perfectly safe have they dumped their deposits into T-Bills.

How is this different than what you described? If the rate increases beyond the coupon of a 10 year treasury, its value drops. Are you referring to extremely short term treasuries?

Thanks for explaining it so well. I was thinking that simply losing the bank was enough in this case, but you make a very good point, and this kind of insight is what's good about this site.

You seem to be conflating the bankers with the bank owners here. The former have done well, the latter have lost everything (total SVB dividends are less than the value of the bank).

Do you really think the owners and senior management of SVB ended up with nothing? What about the stock sales they made right before the FDIC took over, or the bonuses given out, or even their compensation during the years in which this high-risk interest rate scheme was going on?

They have orders of magnitude more money than most people, and will get away with no liability.

> What about the stock sales they made right before the FDIC took over

Is there a more clear cut case of insider trading? SEC should already been working on that now.

Anyhow, you're arguing that they SHOULD end up with nothing, that is an entirely different subject of its own. Because you're talking about punishment, while I'm talking about deterrence.

Punishment must be enacted from outside after the fact, while deterrence can be innate before it happens. These senior management could have years of cushy job and more equity, and now they have to rely on savings and have the SEC up their ass. It's clear which is more preferable.

Just wondering, if they know for sure that they will be sued afterwards, why would they sale their stocks? Why not do nothing and live with what they already have? Is there a possibility that they can get away with it?

> Is there a more clear cut case of insider trading?

Genuine question, is there any evidence that these trades were out of the norm, rather than a regular portfolio rebalancing that’s common with any employee who receives part of their comp in RSUs?

Honestly I'd like for there to be a decent look-back period to recover the funds from any stock sold ahead of time, as appears to have happened in this instance. Use the proceeds to help make depositors whole.

No proof at the moment, but from what I've read several of the executives conveniently sold a lot of their stock more or less at the same time right before this kicked off. Guarantee at least some of that was some insider golden-parachuting.

I would guess that these executives entered their sales months in advance as is relatively typical to avoid insider trading. You can look this up on the SEC website

And in the case of company failure, perhaps the lookback period should be extended beyond several months. I don't have nearly the financial or legal knowledge to suggest viable policy, but from what we know of how SVB failed it would have likely been visible well in advance of the failure to someone with access to the requisite information.

I don't know why people keep calling out the CEO stock sales, unless we find out something new this was almost guaranteed to have been done pursuant to a publicly filed 10b5-1 plan which has a 30 or 90 day cooling off period and must be filed when they have no material non-public information. So if the CEO could see this coming, anyone else could have too on the basis of the same information.

These things can come at you fast. They probably put in the trade instructions sometime last year and they are not permitted to make modifications to the 10b5-1 when they do come into material non-public information as that is itself insider trading.

Trading (or changing a 10b5-1 plan) while in possession of material non-public information, whether in your favor or not, is insider trading.

I don’t know if your are just ignorant or if your are intentionally misleading people but this system is widely abused. A stock sale can be schedule in your plan at the end of every month and you can elect to cancel a planned sale at any time. The CEO used exactly this type of sham plan to unload his shares. Look at the plan he filed this year and the plan he filed every year for the last three years.

> A stock sale can be schedule in your plan at the end of every month and you can elect to cancel a planned sale at any time.

Canceling a 10b5-1 is not in and of itself a violation, correct, but it can kill your affirmative defense as it jeopardizes the good faith element.

However, they would have had to have entered into the 10b5-1 prior to them coming into material nonpublic information in the first place for it to have been valid at all. My point is they made the decision to sell before they knew what was happening and filed a compliant trading plan.

> I think that's a good enough deterrence against bad things.

Nah. They should liquidate the owner's private property as well to cover uninsured depositor losses. Better than making them whole by printing money and having everyone else pay for it indirectly through inflation.

Do realize that the SVB bankers and shareholders remain completely screwed. This bailout does not save them. Nor will any FDIC bailout.

So the FDIC existing does not change how a bank behaves. From the perspective of the bank, bankruptcy and FDIC takeover are effectively the same thing.

Well that's far from the complete picture. It's not that the gov't is backstopping all bank stupidity -- the new facility simply says that for redemptions, US government bonds and MBS can be valued at face value not market value. Only for the purpose of ensuring liquidity for redemptions

Yes, they keep on inventing all kinds of new rules that effectively transform the assets that banks happen to be holding onto assets that are worth more. It's just printing money in an obscure way.

The bottom line is that letting banks invest their clients deposits, while clients - even startups that even know in advance they will need this money in short duration - will keep on blowing in our faces. It might be mortgage backed securities, or treasuries, or anything else.

It's always the same story: banks are leeching money getting rich from taking risks with everyone's money, and the risk is bailed out again and again and again by the government.

They are given government mandate to be the only way to hold money. And then a government privilege to gamble that money on whatever financial instrument that we currently pretend has no risk. And then when we discover it had risk after all, the government pays for the risk.

All the while, banks were leveraged 10x or 20x on the fake "no risk", paid 0 interest rates on deposits, and got to take all the profits from that risk.

The fact that even startups couldn't co opt away from this madness speaks volumes. They were getting leveraged with 10yr duration instruments with depositors base that they knew is burning cash.

If those startups wanted to buy 10yr bonds with their VC money, they would've done it. But the bank just got permission to gamble their clients money.

It's even worse because more than getting bailed out, the thing these VCs want the most is for the rate hikes to stop. They got to both break the system with their actions and get what they wanted.

They must pay salaries - about 2% of deposits. They must pay interest on deposits - now people are demanding 4%. They must pay some dividends too. So they must invest in something.

What's the point of cake if you can't eat it? You'd have to start charging for having the cake.

The current practice of limited investment is reasonable and helps keep the system self funded without much in the way of account fees. It's not as if banks are investing the funds in the equity market. Appreciate I'm commenting from afar and without emotion but these failures are normal. This kind of chaos makes the system stronger. And I think most commentators can agree that this is largely a symptom of a swift increase in the repo rate shortly after significant bond purchases by SVB. There are lessons to be learnt but I don't think if you were sitting on the SVB board and were part of the decision to purchase these low risk bonds did you in any way think it would lead to this outcome.

They didn't have risk officer for months. They lobbied to repeal regulations. And I don't blame them, that's their incentives.

At 10x leverage, when you're correctly assuming your customers will be bailed by the government instead of you getting criminally prosecuted, the worst you can lose is 100% of your money. With the kind of leverage you get in a bank, you don't even need to have positive expectation value investment to have positive expectation value for the bank shareholders.

even with completely trash odds of 50% chance of losing it all and 50% chance of earning only 20% with 10x free client deposit leverage, your expectation value is still 100%!

This is the moral hazard you're dealing with. At 10x leverage ratios of banks, they can take the worst possible bets and still win so long as their maximal loss is just losing all the investment.

You're just encouraging this behavior. This latest decision gives a huge incentives to all banks out there to blow out. Just the incentive structure alone is enough to collapse the entire financial system at this point. It was already eating itself and it's only going to get worse.

It's just a matter of time before they blow it beyond repair.

Why would customers being made whole (at the cost of wiping out all equity and possibly at some cost to other banks) affect the incentives of banks in this kind of situation? What would banks do differently if account holders could lose everything over $250k? If they are happy to “gamble with 10x leverage” then presumably they don’t care about impact to their customers. If bank management risked jail time that might change incentives but doing that doesn’t seem to require a cost to account holders.

Customers should be diversifying in these situations. It’s easy enough to set up a sweep. Those that don’t for whatever reason shouldn’t get bailed out for their poor decision making. That’s de facto subsidizing any future banks that want to make risky investments.

This strikes me as more a perspective of someone whose lived so long in a stable system that they consider it a fundamental immoral failing when something does occasionally go wrong. The loaning of your clients money is the fundemental idea that banking works on, if you weren't able to grow your clients money through lending it you would have no reason to accept clients money in the first place.

Bank runs used to happen all the time. The fact that this is the first bank collapse we have seen in basically a lifetime is more of a miracle than anything else, and should be considered a stunning success that a bank collapse is a once in a lifetime event rather than a yearly occurrence that it used to be.

Define “invest.” Banks invest. That’s literally what they do.

People deposit their money rather than put it under their mattress, and the banks reward them by giving extra money to them.

Then the banks figure out a way to put that money somewhere else that rewards them more than what they are giving the depositors.

The point is, why doesn't the government just capture that revenue? Instead we are letting private companies keep those earnings, without taking on any risk.

Let's deposit at the bank of USA and cut out the middle man.

I see this issue in so many areas. Government orgs and companies have different organizational incentives and tradeoffs. When we substitute a government function with a wallet for contractors, we lose those tradeoff. But it's even worse because now the company has moral hazard.

> Yellen has just broadcast that FDIC insurance is essentially unlimited, as long as you can threaten wider disruption to the economy.

I think everyone knew that already. Since 2008 at least.

It's very possible that if this is not done, the only banks left at the end of the week will be the "too big to fail" ones. A domino effect is very hard to prevent when it's based entirely on consumer confidence and those consumers can very easily create a bank run on literally anything if they freak out.

Not sure I follow the logic. SVB is done right? Saving the companies that banked there is very different than saving the bank. Yes, it might invite more risk by big banks if they know there is a parachute for their clients, but if we close the bank anyways or clear out all parties involved and they have large black marks then there are deterrents (theoretically at least). I like that the gov is acting more like a scrappy company here and getting some shit done when the stakes are high. I dunno, just spitballing here, curious about the counterpoint.

From the perspective of just the people working at SVB, I guess so? But from the perspective of people putting lots of money in one place, it's a reinforcing signal that the most important part of picking a bank is that it be big enough to get bailed out in case of poor planning.

> From the perspective of just the people working at SVB

Who had the former CFO of Lehman Brothers just before it collapsed on their executive team? These people will continue to fail upwards with taxpayer support as they always do.

See you in ten years when he's involved in the next one.

What is the advantage of encouraging people/companies to spread their deposits among multiple banks? Say people were really worried about losing anything over the FDIC limit and so kept multiple separate accounts. Then a bank fails and the government still has to cover the deposits, so what's the benefit? Is the idea that if people are worried about their deposits they won't put more than the limit in banks that are making particularly risky investments? Isn't it more likely though that anyone who would do that would just spread their money out regardless, and therefore there's no disincentive to the banks.

The bank isn't being bailed out though. The depositors are being covered by FDIC in the short term, while FDIC will sell assets seized from the bank. The bondholders and shareholders will take the haircuts. If that's not enough to cover the depositors, banks will be given a special assessment.

The banks left standing will be made to cover the deposits, insured or not, of other banks. It is rather remarkable and I'm not entirely certain it'll work - at what point the special assessment could be unsustainable. Presumably this special assessment isn't instant, and FDIC could just use accounting to make it politically and legally valid to consider it as a non-public and industry financed private bailout.

shrug will it work? I don't know. It really better.

>_shrug_ will it work? I don't know. It really better

The need to be able to field questions like these is why I feel we need open-source economic simultion packages. Does anyone think that people in the individual Fed reserve banks are running anything other than flat spreadsheets to model the financial system? Theyneed to develop economic modeling scripts (at minimum!) a field which is in its infancy. The datascience & modeling capability in HN would eclipse the forecasting power of an econometrics-focused Fed statistical modeling group.

I'd like to see a python library devoted to economic modeling w/ classes for central banks, investent & retail banks, applied into umpteen think tanks' different competing models.

"Yes, it might invite more risk by big banks if they know there is a parachute for their clients, but if we close the bank anyways or clear out all parties involved and they have large black marks then there are deterrents (theoretically at least)."

* As the gp said, it's done. The guarantee isn't new, it's how thing are done now. The Fed is not changing things by doing this, the Fed is doing things as they are expected to be done. Anything else would be changing things, anything else would panic people. Is the Fed "scrappy"? IDK, the "scrappy" efforts to stop crises began with the "plunge prevention team" in the 1990s and have continued more systematically since then, if you want to call that scrappy.

* As to whether there are black marks on people - only the companies who can whether to hire these people later can decide that. Financial companies hire people who've done time for financial fraud so it's questionable what sort of "black marks" the Fed could give if it wanted to (People mention the Lehman guy but was Lehman really worse than the others in 2008 or just a scapegoat - like fricken Martha Stewart. Was that guy involved in excess or just a random manager? I recall he was now managing a stock subsidiary that's being spun-off whole. But still).

> It's very possible that if this is not done, the only banks left at the end of the week will be the "too big to fail" ones.

I don't get it. Doesn't the unlimited FDIC insurance encourage mega-banks? If funds were only insured up to 250k, wouldn't that just mean we would have to spread money across multiple banks. And sure some banks would be wiped out but new better banks would take their place. It's not a closed system

Banks used to fail and be smaller failures. Now we removed almost all failures except when we have a failure its huge:

It's like forest fires, we shouldn't build fragility into the system by removing all risk and then rely on regulations to mitigate it. Hasn't worked in the past and will lead to more consolidation and bigger fires in the future. Remember in 08 the answer was to combine a bunch of banks and since then we've had no new banks created (besides Ally which was a spin off of an auto workers pension fund if i remember)

That estimate is misleading as SV failed after people pulled 45 billion out. It wasn’t a 200 billion dollar bank when it failed and people didn’t lose 200 billion dollars.

We are at ~1.3 bank failures per month in 2023 which is much closer to 2020’s 0.3/month than 2009’s 11.7 banks failing per month. That IMO says more about the rest of the year than the size of the banks that failed.

The parent comment just made the point that you need to normalize for the size of the bank, not for the number of banks per year.

Your comment takes the annual frequency and divides it by 12 to get an average monthly frequency, adding nothing to the argument of the grandparent comment.

They suggested you should normalize for the size of the bank but didn’t support it. They even used non inflation adjusted numbers.

Maximum assets under control don’t correlate with actual losses especially when people pulled money out before the collapse. It’s a completely meaningless number on it’s own.

Certainly very valid criticisms. To be fair, I specifically was trying to ballpark it and this graph does not contain the Signature failure yet so I think it is a fair representation of this particular metric.

I also think it's a good point that a dollar is not necessarily equal to another dollar in this context. But the same can be said for individual banks as well.

I put the majority of my cash in one of the smaller banks. The news that has transpired in the past few days had me mulling moving those funds to a larger bank, likely Chase (one of the too big to fail ones).

Even with the FDIC guarantees, I was not at all confident that :

1. they actually had the funds to cover _many_ bank runs; and

2. it won’t take weeks if not months for me to recover my funds, if my bank fails.

It’s entirely possibly that these lines of thoughts will motivate many more people to consider this exact move, putting even more stress in the system.

The FDIC is backed by the full faith and credit of the US government. If a bank fails, your insured deposits will be made while, usually the next business day.

The US government has a debt limit. The government is going to run out of options for not exceeding that limit in a few months unless it is raised. There are people in congress suggesting that they should let the limit get hit. If the debt limit is hit, do you e pectin the government to be able to pay out FDIC money in a timely manner?

Not just FDIC though, in 2008 and again today the Fed is making clear that their backstop is bigger than just FDIC. it can’t be any bigger than the debt limit so I find it sobering to have this discussion while we’re heading towards that cliff.

With the Bank Term Funding Program, people who moved or previously kept monies in large banks have less incentive to do so, until 2024 when this program is scheduled to end. That is, if they think 25 billion is enough to prevent more runs, and the FED/treasury/FDIC will not greatly expand that in the event of another run.

IMO you should probably do business with multiple banks with somewhat separate market segments to try and diversify risks. You shouldn't have all your cash under one mattress ;)

Imagine you’re a business owner. Would you rather bank with Local Community Bank, the failure of which will essentially kill your business, due to haircuts on uninsured deposits that’ll annihilate your working capital, or will you bank with Chase, the failure of which forces government action to cover depositors because the economy is a goner otherwise?

But isn’t your CFO planning for financial risk? Do you have hazard insurance on your leased offices, what happens if one of your key employees is unavailable, a large customer is late on payment, you get hit by supply chain issues, etc.

You can’t seriously tell me that the CFO who is responsible for corporate finance at these SVB customers didn’t realize a business checking or savings account is not fully guaranteed? It’s in every single bank brochure and statement. If that’s that case, they need to suffer the consequences of poor contingency planning.

Isnt then the whole thing fault of VCs who included those covenant? The same VCs that now cry hardest?

Moreover, both startups and VCs are literally the groups that celebrate risk taking and disruption. This is it, this is the flip side of risk, the definition of risk is that you might loose. But somehow, when they loose, due to risk taking, then suddenly they want extra bail outs and help.

According to the AP, there was a second bank failure today (Sunday) and there was a risk of a third:

> In a sign of how fast the financial bleeding was occurring, regulators announced that New York-based Signature Bank had also failed and was being seized on Sunday. At more than $110 billion in assets, Signature Bank is the third-largest bank failure in U.S. history.

> Also Sunday, another beleaguered bank, First Republic Bank, announced that it had bolstered its financial health by gaining access to funding from the Fed and JPMorgan Chase.

That article is already out of date. Signature Bank also failed today.

I suspect that Signature Bank's failure is tied to their crypto activity. But the sight of 2 banks failing while there was an ongoing run on at least one more bank does seem like the kind of thing that could start a panic.

The entire regulatory system encourages mega-banks. The entire “too big to fail” concept encourages it. Complex regulations benefit those who can afford the legal costs of compliance. Dodd-Frank probably made this outcome more likely.

The role of the government in letting this happen has been under-covered so far. Weren’t they supposed to be overseeing things, stress-testing banks, etc? Regulators either were not looking, or were looking but did not notice. Regardless, there is not much sense to the argument that the government is “stepping in” tonight, because it was always involved.

Has nothing to do with flooding the world with cheap money which chased unrealistic yields. Systemic excess liquidity when deposited needs excess assets to balance. Assets which were bought at inflated prices. The question now is only how much will this house of cards collapse.

That didn't prevent multiple runs against Washington Mutual in 2008, and it won't prevent runs now. People are worried that they won't be able to get to their money even if it is insured.

Plus, even if the "typical" consumers don't freak out, businesses might. There are a lot of businesses with accounts over the FDIC limit. Only about 60% of bank deposits in the US are insured.

If I thought the US government was going to fail I'd simply try to be the first to convert my dollars to a dense and valuable commodity, like gold, and then find another government to live under. It's not like people pulling out dollars have to keep their wealth in dollars.

How would they even do that? Bitcoin handles ~350k transactions per day. VTI (Vanguard's Total Stock Index), a large size fund is on average traded 3,670k per day. That's one fund. There is no reasonable way for small customers to pull out of index funds to bitcoin unless there is a fundamental change to how bitcoin operates.

Small customers get BTC from an exchange, which keeps their accounting internally. No transaction volume limits.

Later the small customer may move that BTC to self-custody, which could be an on-chain transaction or LN or other side chain with more transaction capacity.

And perhaps there's no other way? The Japanese did the same with their overpriced real estate provlem, Europe did the same with their almost defaulting countries.

Think about who gets hurt if the banking system collapses. It ripples out into the rest of the economy, because in fact the economy runs on debt. It would be harder to maintain existing businesses and start new ones if there was a credit crunch -- we lived through a credit crunch after 2008 and it was very bad for everyone.

Even if you want certain people to get hurt by this (and there is definitely a baying mob that seems to want to cause as much suffering as possible because they just don't like certain classes of people), keep in mind that this could cause a 2008-style recession that hurts everyone.

Who do you think gets hurt more by an economic downturn? The billionaires who lose millions and end up still being rich, or the working people who lose their jobs and can't afford housing? This isn't a theoretical question, we know the answer because it happened before.

I have some off-the-grid and expat friends who I suspect are rooting for a collapse primarily to justify all the shit they did and said. These types seem to thrive on doom and I have no doubt they've always existed throughout history.

Eventually I suppose they'll be right, but primarily as a result of one of those broken clock coincidences ...

The desire to let it all burn comes from those who played by the rules.

The government's intervention creates moral hazard: those that played with fire got burnt, and those who didn't didn't, but those who didn't get burnt were positioning themselves to take advantage of the opportunities that the crispy bodies would have generated.

But the government swooped in and saved the crispies, without penalty to them, at the cost of those who had proper risk-adjusted positioning.

We see this time and time again. The government is changing the rules after the game is over to change the losers to winners. It's nonsense.

Sounds similar to when people were rooting for airlines and auto manufactures to just die in 2008 to say "fuck the rich". I'm glad they were all saved.

In human psychology, fairness is a big driving force in society. I think studies have regularly shown that people will tolerate outcomes that are objectively worse for themselves if the alternative seems unfair but objectively better.

People are not rational. Homo economicus is a myth.

Isn't spite just wanting that version of karma or justice but hurting yourself in the process. If we let these banks collapse it's definitely going to hurt lower income people more than wealthy people so to me that is 100% spite

No. Spite is hurting yourself to hurt someone else. A desire for karma is willing to hurt yourself for justice. They look very similar, but are different.

That is incorrect, spite is seeking the deliberate harm of another. It’s possible for spite to include hurting yourself to inflict it, but that’s not in any way necessary.

Sure, and karma doesn't require hurting yourself either. I meant in the specific case we were discussing, in which harming yourself was already baked into the situation. I admit I could have been clearer initially and am sorry I spoke clumsily.

Justice is the idea that people are treated equally, impartially, and fairly under a set of standards. If someone breaks the rules justice is them getting the same punishment anyone else would get, concerns about externalities don’t come into it.

Is everyone getting hurt ideal? No. But that’s a different question than is it justice.

IMO this is what happened during 2008. The government tried to minimize harm at the expense of justice, and people are angry because they don’t realize how bad it could have been.

If the two options are a) everybody except the rich get hurt and b) everybody including the rich get hurt, then I think the majority of Americans would go with b.

B is definitely where we're at. Many Americans are tired of watching the rich get bailed out with socialism-for-the-rich-not-for-the-poor. Meanwhile the not-rich continue to struggle in every aspect of life, from food to housing. And blame is placed squarely on the rich, who have a greater voice in the elected government.

No. That is called crony capitalism. True capitalism would let these banks burn and allow those who saved or have capital buy them up. No gov intervention allowed.

No, it's just called "capitalism". The thing you call cronyism is a core feature, not a bug: under capitalism, the capitalist class advances its own interests.

Please stop trying to redefine basic terminology to suit your agenda.

Yes, but we're disagreeing about the specific meaning of words. Capitalism describes an economy where capital is the mechanism through which goods and services are allocated. It is not the partnership of public and private entities, as you suggest. That would be crony capitalism.

That page describes how "crony capitalism" is used colloquially. Dictionaries are not a great source for determining canonical meaning of complex political terminology.

I argue that usage of the term "crony capitalism" is itself a form of capitalist ideology.

The socio-economic system where social relations are based on commodities for exchange, in particular private ownership of the means of production and on the exploitation of wage labour.

Wage labour is the labour process in capitalist society: the owners of the means of production (the bourgeoisie) buy the labour power of those who do not own the means of production (the proletariat), and use it to increase the value of their property (capital). In pre-capitalist societies, the labour of the producers was rendered to the ruling class by traditional obligations or sheer force, rather than as a “free” act of purchase and sale as in capitalist society.

Value is increased through the appropriation of surplus value from wage labour. In societies which produce beyond the necessary level of subsistence, there is a social surplus, i.e. people produce more than they need for immediate reproduction. In capitalism, surplus value is appropriated by the capitalist class by extending the working day beyond necessary labour time. That extra labour is used by the capitalist for profit; used in whatever ways they choose.

The main classes under capitalism are the proletariat (the sellers of labour power) and the bourgeoisie (the buyers of labour power). The value of every product is divided between wages and profit, and there is an irreconcilable class struggle over the division of this product.

It probably doesn't need to be said, but it's pretty obvious the bias in that definition.

There is no singular definition of capitalism, but many others would differ on the distinction you've drawn from earlier posts. E.g., a system based on the reinvestment of excess profits does not necessarily equate to crony-capitalism. It seems your issue is with the person using the word "socialism" to describe a social ill of crony capitalism. But there is a distinction there that is being muddled in the conversation.

Can you coherently define "crony capitalism" and explain how it's not a fallacious no-true-Scotsman defense of "real capitalism" (or whatever term you prefer)?

Capitalism disallows private and public collusion beyond what is necessary to ensure public goods, defined by those gods which are nonexcludable and nonrivalous.

How does capitalism "disallow" any of that? Where is your evidence that disallowing this is a stated goal under capitalism?

I think you're confusing "free market" USAmerican right-Libertarian ideology with capitalism itself.

Capitalism, simply put, is defined as private ownership over the means of production, and the people who have that ownership are called the capitalist class. None of that precludes any sort of collusion.

Such collusion (and other things, such as child labor) was commonplace in the Western world recently and is still commonplace elsewhere — capitalists still wail and cry foul when legislation, no matter how toothless or perfunctory, is introduced to curtail such behavior.

You’re confusing what is a central tenet and what may occur as an outcome of a poorly executed version of the principle. By that same logic, tyrannical despots could be argued as a stated goal of socialism.

I don't think those are the only two options though. b) The rich now have less billions but still billions and everyone else now has to budget even harder.

There was no guarantee that the govt will make money but there is a guarantee it creates a moral hazard. If you are a banker take excessive risks and enjoy the profits, if things go wrong, the govt will bail you out.

Heads I win, Tails I dont lose.

You also ignored that govt/Fed keeps printing more money, so the taxpayer ultimately loses with inflation.

>At the same time, this is yet another example of changing the rules in the middle of the game. Yellen has just broadcast that FDIC insurance is essentially unlimited, as long as you can threaten wider disruption to the economy.

No, there are systemic risk exceptions within the rules. If a bank is large enough, then the systemic risk to the economy as a whole is large enough to warrant this step. "Too big to fail" is typically a derisive comment, but it is not without practical reason. Governments are supposed to act in the best interest of the governed. I hope it is clear to all of us that avoiding the economic disruption of a cascade of bank failures is in our interest.

Smaller bank failures do not pose systemic risk and so they will not be backstopped in the same way. Might seem like unfair treatment, but practical concerns often outweigh the theoretical. By the way, SVB is still a failure and as a company is now gone. Some other entity will take over its assets, debts, and customer services. All senior management has been removed.

>I understand part of this is human nature but I really wish we could plan for these entirely foreseeable events ahead of time so that it's not just cases of "selective justice" with regards to who gets bailed out.

We did. That is why we have the FDIC, the Federal Reserve, and the Treasury department. They did their job and did it quickly and effectively. SVB did not get bailed out, the depositors did.

Is it though? I think there's a proportion of readers who might feel grifted by regulatory capture (eg: unable to get on the housing ladder due to draconian zoning policy) and reasonably feel that some of the moral hazard has to be addressed to stop what has been unstoppable growth to give them a chance to establish financial security. It's a fallacy to see it as zero sum, but a temporary crisis in confidence might produce the only opportunity in a lifetime to create the conditions needed for affordable housing to be available for purchase for folks who can keep their jobs during the crisis. Many feel economically abandoned.

You can't just snap your figures and have the housing market drop by 60% and keep everything else the same.

Those same people are going to lose their jobs and burn through all their savings and be unable to secure loans to buy houses.

Even if you bank at a supposed safe and secure credit union, a systemic crisis will affect them as well. You won't be able to get a loan. There goes your opportunity.

The whole financial and economic system is intertwined and you're part of it, if it blows up and crashes into the rocks, you're going down with the ship as well. Get over your Main Character Syndrome where you think you're going to be the one immune to the catastrophe.

I know many good, hardworking people who secured their position on the housing ladder in the aftermath of the global financial crisis. In conversation, they were bewildered by how much their homes appreciated even by 2018, well before the pandemic bump in valuations.

But is anything being done about it? It is both unequality and bananism at its best. You give money to the "rich" (though this time indirectly), you encourage recklessness and you also change the rules when you see fit.

All of these described above are "disrupting" the economy. And none of them is in our interest.

The really rough part about HN is the low level of knowledge about how governments and politics work. It's ok to judge these outcomes harshly but many commenters here intermingle their judgements with their mental models that seem to have not evolved beyond what they were taught in secondary school.

It's really quite concerning because some of these people have tremendous power. I suppose the only positive is that a number of titans of Silicon Valley are not savvy enough to challenge increasingly assertive governments.

While what you say is true, maybe we shouldn't allow mergers and other avenues to allow these banks (and other verticals) to be too big to fail. We've made that a target for all companies. Just get too big to fail and you get all the upside and none of the downside for free. That is my main complaint. By allowing deposits to be invested without risk, these too big to fail banks are encouraged to chase the highest yield, highest risk re-investments possible. If it works, another yacht for everyone! If it fails, we must be made whole!

I think at least a part of the solution is to increase regulation as banks get larger. Since it is clear that the fate of very large banks is tied in to the the fate of the economy itself, they should be appropriately regulated. In particular, short term asset/deposit ratio requirements should be modified as a bank gets larger. That could reduce the need for the FDIC to step in when depositors get nervous and provide disincentives to getting too large.

I think something like this could make large banks more of an asset for the economy rather than a liability. I wouldn't want to just set a maximum size. If a bank wants to get huge and maintain conservative and safe asset/deposit ratios, good for them.

The problem is that guaranteeing a bank and regulating it's investments still changes the incentives for the bankers. The banker has an incentive make an investment that can presented as "prudent" but which actually has a large up and down side. The banker keeps the upside, the bank's depositors are protected from the downside and the worst the investors face is losing their existing capital.

I would argue no. The issue is that the FDIC has deposit insurance limits already. The depositors are free-rolling on the amount they are getting made whole on above the limit. Then you are just encouraging some new kind of "bank" with limited access to become a customer (e.g. > $50M deposit) and then you can just put all "shareholders" in the role as customers. You are still giving free upside outside the rules that all other depositors are stuck with. Every investment comes with the statement: "Investment contains risk". If the bank wasn't leveraging these deposit as investment cash, there would have been no collapse.

You're right this produces risk but you're wrong about exactly how.

Any bank call pull in deposit and use them as capital. But being a customer also doesn't give one any particular upside - you just get interest on the money you deposit. And if you have a special bank with only large deposits and paying extra high interest, then regulators look at you and quite likely see something not to be protected in the same way.

The way you get risk is basically the way SVB did it. Share holders can lose at most their entire capital but they can get to play with all the money the depositors give them. If they bet on something that pays off big, they get that payoff minus the modest interest they pay depositors and if they lose, they lose at most their capital.

If you can use just a bit of capital to borrow a whole lot of capital, with the only risk to you being your original capital, then you can engage in very risky ventures, getting a huge payoff if you succeed and at worst losing your original capital if you lose.

Come to think of it, that seems a bit like what SVB did. Buying long term bonds when interest rates were likely rise seems like a recipe for disaster - and in fact the logical outcome was this bankruptcy. But there was a chance that interest rates wouldn't have risen, at which point the shareholder get a big payoff, pocket it and go on to the next risky maneuver.

> > Governments are supposed to act in the best interest of the governed

Many of the governed see what policymakers and politicians call 'systemic risk' and 'instability' as a not so unwelcome wildcard considering that the wealthy of today are mostly descendants of wealthy land owners from the times of the Crusades.

> > They did their job and did it quickly and effectively

Where are the Fed , D.C. , the FDIC etc. when a gas station goes belly up? Or a small family owned boat builder in Maine? Nowhere to be found. Their fault? Not being systemically important enough. Whatever the fuck that means.

> Many of the governed see what policymakers and politicians call 'systemic risk' and 'instability' as a not so unwelcome wildcard considering that the wealthy of today are mostly descendants of wealthy land owners from the times of the Crusades.

I'm curious if you have a citation to support that the wealthy in the US are descendants of wealthy land owners from the times of the Crusades at a substantially greater rate than the general population.

> Where are the Fed , D.C. , the FDIC etc. when a gas station goes belly up?

How much of their going belly up was due to Fed policy? Particularly driving and holding interest rates to near zero through market actions then pushing interest rates to nearly 5%?

Read over the history of the US settlement. While they came from the UK and Germany, the vast majority are not descendants of the Normans.

One of the major draws to the US has always been the opportunity to do a little crusading of ones own and find whatever opportunity your courage and lack of scruples allowed you to get away with.

In cases where you can't predict the future appropriately, sometimes it's better to make prudent decisions that help everyone instead of attempting to punish the sinful.

Keep in mind that bank shareholders and senior management are going to get wiped out and fired.

I mostly agree with this, but I feel like the past 25 years or so, ever since "the Greenspan put", has just gone more and more in the direction of telling people that they don't need to worry about doing adequate risk assessments, because if you have powerful people that yell loud enough, and you can cause enough damage, that Washington will come to the rescue. Eventually, I just don't see this ending well.

As someone who is naturally risk averse, I feel like a sucker. I was having a conversation in a separate thread where someone remarked "How can you expect startup companies to spread their deposits across multiple banks?" Besides the fact that there are tons of account structures specifically set up to do that, as an individual, I know what these insurance limits are and have moved assets around accordingly (for me, FDIC limits weren't relevant but SIPC limits were).

How much time I wasted. I should have just gone with a powerful enough institution that I knew would get bailed out if they ever failed. I certainly won't waste my time doing this again, which is probably not the follow-on effect that the feds want.

The decisions about "is this bank adequately capitalized to serve its depositors" should be made by the regulators, not by the market. We know what it takes to run a bank safely, and its really easy to both quantify and test. This is how the "too big to fail" banks are run today. No one talks about the moral hazard of elevators (make sure you inspect it before you get on) or airplanes (make sure you do your own pre flight check) we trust that the regulators have set up processes that make this infrastructure safe for the public to use. Even with a deposit guarantee, a poorly run bank can still be closed by regulators, a bank run doesn't need to happen for a bank to be shut down, just like an elevator accident doesn't need to happen to decertify an elevator in a building.

It doesn't take a CPA to know that depositing above 250k comes with increased risk. And I think you're kind of conflating types of consumers here. People depositing above that limit are generally not working from the same limitations and lack of information that regular people are.

Companies need to run payroll twice a month. $250k is about one months payroll to 25 people. Many companies are a lot larger than that. You also have planned and unexpected expenses and other payments. Many payroll and providers also require you to set up one account where the funds are pulled.

You don’t want to move money around every week, so you keep heathy balance.

It’s also never adjusted for inflation, despite this mess in theory being triggered by raising of interest rates due to super high inflation. 250K when it was set in 2010 is the equivalent of almost $350K now. If we ignore that, then we’re just admitting the number is totally arbitrary and we shouldn’t even bother arguing whether it’s a lot or a little.

Separately, it’s weird that a joint account is insured to 500K but a business account stays at 250K. It actually does weirdly favor wealthy individuals vs. working capital accounts for businesses that might represent many employees.

The sentence clearly means that it was never adjusted from inflation from when it was adjusted to 250K, 12 years ago. You can tell that this is far from being adjusted for inflation since it is now 100K off from what it was in 2010, or 40%. This should be a "neutral" issue with respect to the SVB thing, pegging it to inflation helps everyone in the system.

Obviously people have different salaries but also are payroll taxes and other taxes or fees that also need to be paid like unemployment insurance and whatever else the local government has decided. Sometimes these are collected city/county as well as at state level.

Benefits also cost $500-2500/mo (if you cover 100% employee and 70% dependents).

Not complaining but just saying there are costs that are not always apparent to employees.

also rent, servers, the cost of anything else you have to run your businesses. For broadly generic tech companies, take everyones top line salaries, double them, that is your rule of thumb monthly expense line item that wraps everything up (rent, taxes, the cost of doing business, marketing spend, etc)

Yes, that is a lot of cash for an individual. I don't really know why anyone would sit on a lot more cash than that without at least putting a healthy portion into Treasuries or other durable assets.

For businesses, it is a trickier proposition but there are reasons that companies roll cash into assets and operate largely from credit.

Consider financially responsible people in their 50’s and 60’s that have had decades to save. There are plenty of “regular”, middle class people with this type of savings in their account.

If you have that much in liquid cash, you meet virtually no definition of the term "middle class". You are upper middle class at leadt and you probably have a financial advisor who is telling you that you shouldn't locate all your money in one account unless it is yielding in a way that justifies such a risk. At least I hope you do.

Yeah, that's actually about what I make but let's be real, this is a very small number of people. I have a financial planner.

Are there people in this asset class who aren't getting financial advice? Yes. But it's not like ma and pa kettle are getting wrung out by the savings and loan here.

At this point we should just nationalize the whole banking system. Currently we have the worst of both worlds: privatised profits and socialised losses; strict regulations but limited oversight or appeal; no real market competition but no real voter influence either.

we don't have "socialized losses". Tax payers aren't paying for anything here. The FDIC is run an funded by an interbank consortium. Its essential a union of banks that run a collective risk pool and decide the rules of the risk pool. It works and has worked for nearly 100 years.

> we don't have "socialized losses". Tax payers aren't paying for anything here. The FDIC is run an funded by an interbank consortium. Its essential a union of banks that run a collective risk pool and decide the rules of the risk pool.

What meaningful distinction are you drawing here? It's not practical to opt out of banking, and FDIC has no real competition (the NCUA offers exactly the same terms, and in the credit union thread fans were at pains to emphasise how equivalent to the FDIC it is). Not all taxes are collected by governments from individuals.

Consider: “Reserve requirements are a tool used by the central bank to increase or decrease the money supply in the economy and influence interest rates. Reserve requirements are currently set at ZERO as a response to the COVID-19 pandemic.”

ref: https://www.investopedia.com/terms/r/requiredreserves.asp

I don't think it necessarily is adjusted for risk that specific banks take on as operators. It's likely set at some requirement to help the fed achieve its goal while also adjusting for median or 2 std dev risk.

I prefer to minimise banking's influence over everything, because banking is itself a form of political regulation - but not a democratically accountable one.

at the end of the day, everything in life is political.

Did you also consider that the political incentive for a regulator are at odds with the ones running the bussiness. (mainly, not getting people killed).

I've been a student of housing bubbles for a long time. I remember back in 2003 I was participating in an online forum covering the bubble. The conventional wisdom back then was that when the bubble popped not even the Fed or Alan Greenspan and his helicopters could cover the losses. The hundreds of billions if not trillions of dollars that would be needed would cause runaway inflation.

Then, they did it. The bastards managed to somehow buy tens of billions of mortgage backed securities every month for years. They bailed out automakers and banks with backdoor 0% loans while claiming the "investments" were profitable for the average citizen. Zombie Fannie and Freddie are still out there gobbling up mortgages. It's insane.

None of this is surprising to people who know how bank money actually works. The US congress literally has unlimited nominal credit and practically unlimited useful credit, and it can grant same to any of its creatures.

Of course they could, money is a fiction after all. As long as we all keep walking around believing that fiction, there's no real problem with just inventing more money out of thin air.

The fiction has certain properties when it encounters the real world though, so there are sometimes downstream consequences, but none that could ever totally dissolve the fiction. Only enough people starting to disbelieve in the fiction itself could do that, and people mostly won't do that because money is too useful.

Well if I don't produce that fiction on demand for something called "taxes" I get put in a cage or even killed by men with guns. So I'm pretty motivated to go along with the fiction until the men with guns stop making me.

Why isn't it. Pragmatically it's pretty silly to insure the first 250k and then expect people to go through the trouble of spreading their cash over a multitude of accounts. Punishing people for not having accounted for black swan events in their risk assessment is also not scalable. Do we want people to do useful stuff, or to spend their time digging the rule book to ensure they've accounted for every eventuality?